The food industry is highly competitive and offers little opportunity for differentiation. Most companies essentially act as middlemen between food crop producers (farmers) and consumers. This leaves firms exposed to increasing costs from rising agricultural commodity prices, and constrained by the inability to hike product prices without facing pushback from cost-conscious consumers. Companies that have established brands are able to charge higher prices to consumers, but customers can be fickle. Creating an established brand is also a long-term commitment, and it involves substantial marketing and promotion expenditures. The retail food industry has been undergoing a period of consolidation, creating larger and more sophisticated buyers that yield more market power over the food companies.

In this article, let's take a look at three players in the food products industry:

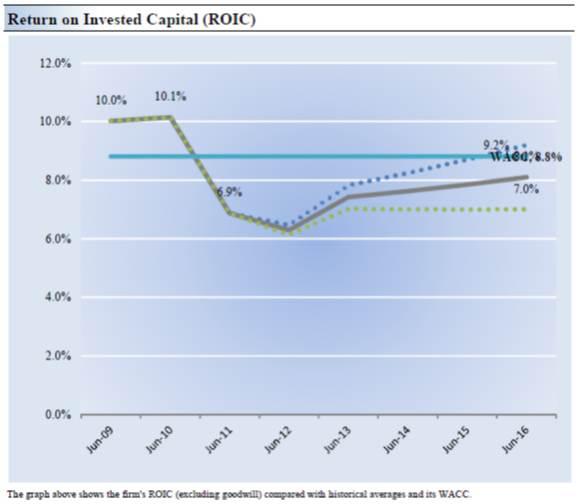

Archer Daniels Midland

Archer Daniels Midland Company (ADM), which makes a variety of value-added food and feed ingredients (protein meal, vegetable oil), operates in a very weak competitive position, in our view. The company is unable to either raise the price of its products or lower the cost of its agricultural raw materials compared to the market price (absent hedging, which can be duplicated by other firms). Agricultural commodity prices are also highly subject to government policies and mandates (such as import and export restrictions), which are out of the company's control. Further, because its products are also commodities, product pricing is also partly dependent on the industry's processing capacity, which in turn, is determined by the actions of its competitors. Rising input costs and the inability to raise product prices is a persistent problem that will continue to impact the firm's profitability. The large decline in the company's return on invested capital to 7% from 10% during the last three years is an indication of its extremely weak competitive position (please see chart below):

(click images to enlarge)

Tyson Foods

Tyson Foods (TSN), which produces, distributes, and markets chicken, beef, pork, and other prepared foods, has weak competitive strengths, in our view. Though the firm is one of the world's largest meat processing companies with recognizable brand names, its input costs are highly dependent on fluctuating commodity prices. And while the company retains some power to charge higher prices for its products, its customers (such as supermarkets and food distributors) continue to consolidate, and this trend is expected to persist in many of its major markets. Such consolidation has created larger and more sophisticated customers with increased buying power, reducing Tyson's ability to raise prices. Further, the food industry is subject to changing consumer trends and preferences. Though excess returns over the long haul will be hard to come by, we think Tyson's valuation looks attractive at current levels (please view our assumptions below):

ConAgra Foods

ConAgra Foods (CAG) has moderate competitive strengths. The company is one of North America's largest food companies, and it is focused on adding branded and value-added businesses, while strategically exiting commodity-based businesses. Though ConAgra's strong brand name may allow it to set higher prices than those of its competitors, the firm's ability to increase prices at will remains constrained by customers. Further, retailers are gaining market power by consolidating into larger companies and developing their own branded and private-label products. ConAgra remains dependent on the relationships with many of its key customers, with Wal-Mart (WMT) accounting for about 17% of the firm's revenues. Still, the firm's return on invested capital has held up better than most, indicating a stronger competitive position than its peers (please see chart below):

Source: Seeking Alpha (http://goo.gl/TaIje)

Aucun commentaire:

Enregistrer un commentaire